Q1 GDP - Not as bad as it looks, yet

Q1 GDP - Not as bad as it looks, yet

A contraction versus expectations for slight growth, but the details are less grim

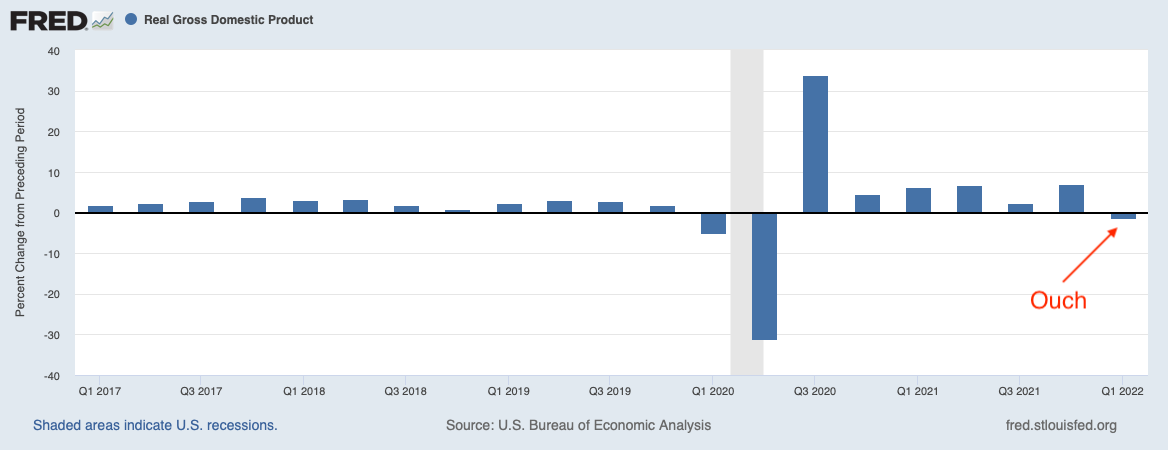

Today’s first estimate for Q1 2022 GDP was a stinker, with annualized real GDP coming in at - 1.4% versus consensus expectations of around +1.0%. This was the weakest headline since the dark days of Q2 2020, but the details aren’t quite as bad as the headline. There were three significant areas that hit GDP hard:

Net exports cut 3.2 percentage points.

Inventories cut 0.8 percentage points.

Government spending cut 0.5 percentage points (to be expected after those massive stimulus programs)

Remove these three, and we get 3.5% annualized real private domestic demand.

There is a bit more to the story, though.

US goods deficit rose to a new record high of $125.3 billion in March, well above expectations for $1.05 billion, and this comes after $106.6 billion in February. Overall in Q1, the deficit widened by 20%.

Despite all the complaining about supply chains, imports rose 11.7% in March, the second-largest increase on record, and are up 26.7% YoY.

Consumer goods imports rose 13.7% in March, the sixth consecutive increase to reach the highest level on record.

Putting all that together and Q2 looks to be facing a potential excess inventory headwind.

On the positive side:

Capex rose 15.4% annualized - this is likely to remain strong

Non-residential construction rose 9.2%

Residential construction increased by 2.1%

Consumer spending rose 2.7% annualized. That looks good, but call me cautious when we see rising credit card balances in light of falling household income to fund that spending.

Speaking of debt

Mortgage applications have been falling hard for seven consecutive weeks and are down 51.4% YoY while refinancing is down 70.8% YoY. That’s got me speechless, and that’s not easy to do.

The full-economy debt-to-GDP ratio is around 350% right now, versus where it was at the start of previous Federal Reserve hiking cycles:

1983 170%

1988 235%

1994 260%

1999 305%

2015 325%

Increases in interest rate will subtract more from GDP as the cost to service that debt rises.

With public and private debt at a record high of $83 trillion, if rates do climb to 2.7% by year-end (as is predicted by the OIS market), debt service would grow to around 1.5% of GDP or $330 million.

Talk about a headwind.

The Fed is gearing up for the fastest pace of tightening in nearly thirty years, and before it even gets started, the economy has already contracted. This is going to be a bumpy ride.